Nvidia at the Center of the AI and Geopolitical Storm

Few companies embody the intersection of artificial intelligence, global politics, and market dominance quite like Nvidia (NVDA). Once a niche graphics card maker, Nvidia has transformed into the most valuable semiconductor company in the world, powering everything from AI training models to autonomous vehicles.

Yet, as its valuation soars past $4 trillion, Nvidia faces challenges from both rivals like Huawei and the ongoing tug-of-war between the United States and China. With regulatory scrutiny, geopolitical uncertainty, and Wall Street optimism colliding, investors are left asking: Is Nvidia still a buy now?

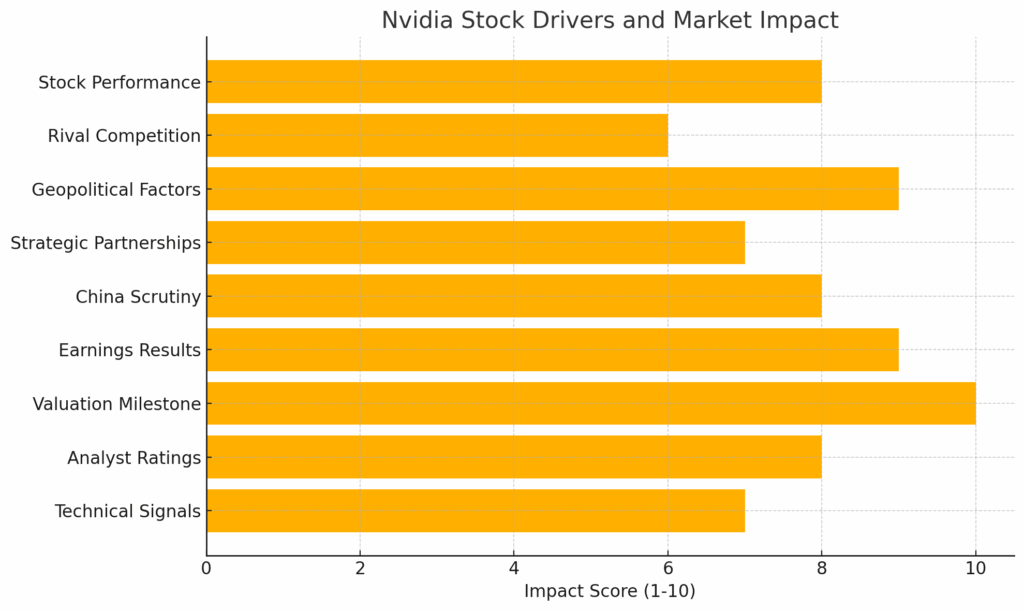

Nvidia’s Stock Performance: Riding High but Facing Headwinds

On Friday, Nvidia stock hovered just above a key support level, ending the week with a 1% decline. This pullback came after a 6% rally the prior week. Currently, NVDA is trading in a flat base pattern with a buy point at 184.48 — also its all-time high.

Despite the dip, Nvidia remains one of the best-performing stocks in the AI sector, having surged dramatically over the past year thanks to relentless demand for AI chips.

Huawei’s AI Push: A Potential Rival Emerges

According to reports from The Wall Street Journal, Huawei is ramping up efforts to develop its own AI chip pipeline. While Huawei’s chips may lack the advanced capabilities of Nvidia’s, the Chinese tech giant aims to bundle networking technology with chips, boosting overall computing power.

This strategy highlights China’s determination to reduce reliance on U.S. semiconductors, especially amid trade restrictions. While Huawei may not dethrone Nvidia soon, its AI expansion signals growing competition in a space where Nvidia has long dominated.

Trump-Xi Call: Political Moves That Could Impact Nvidia

The geopolitical backdrop is just as important as technological competition. On Friday, President Donald Trump and Chinese President Xi Jinping held a phone call after several days of high-level talks in Madrid. Any developments in U.S.-China trade negotiations could directly impact Nvidia’s business in China, which remains a sensitive and lucrative market.

A more cooperative trade outlook could benefit Nvidia, while tougher restrictions may limit its ability to sell high-end AI chips overseas.

Nvidia-Intel Collaboration: Expanding Strategic Partnerships

Adding to the intrigue, Nvidia and Intel (INTC) recently announced a collaboration to develop custom data center and PC products. Nvidia also revealed a $5 billion investment in Intel’s common stock at $23.28 per share.

This move positions Nvidia not just as a competitor but also as a partner with legacy chipmakers. However, the deal requires regulatory approval — another hurdle given current U.S. oversight in the semiconductor industry.

China’s Regulatory Scrutiny on Nvidia

Nvidia’s relationship with China has grown increasingly complicated. This past week:

- China’s Cyberspace Administration ordered major tech firms to halt purchases of Nvidia AI chips.

- China’s State Administration for Market Regulation launched an antitrust investigation into Nvidia’s 2020 acquisition of Mellanox Technologies.

While Nvidia insists it has obtained all necessary approvals for past acquisitions, the mounting regulatory scrutiny poses long-term risks to its China strategy.

Wall Street Optimism: Analysts Raise Price Targets

Despite the political uncertainty, analysts remain largely bullish on Nvidia.

- William Blair’s Sebastien Naji gave the stock an outperform rating with a $205 price target, noting potential upside despite zero revenue expected from China in Q2.

- Susquehanna’s Christopher Rolland lifted his target to $210 from $180, though he cautioned about revenues tied to Nvidia’s H20 chips.

The mixed sentiment highlights how Nvidia’s global challenges coexist with its dominant fundamentals.

Second-Quarter Earnings: Nvidia Beats Expectations

Nvidia reported fiscal Q2 earnings of $1.05 per share, topping estimates of $1.01. Revenue came in at $46.74 billion, also beating forecasts of $46.05 billion.

For Q3, Nvidia guided $54 billion in revenue, slightly above Wall Street’s expectation of $53.43 billion. Importantly, the company excluded sales of H20 chips to China, underscoring regulatory challenges.

In addition, Nvidia announced a $60 billion stock buyback, reaffirming confidence in its long-term growth.

The China Revenue Deal: Controversial Agreement Raises Eyebrows

A recent development stirred further debate: Nvidia secured a license to sell H20 AI chips in China but agreed to give 15% of its revenue from those sales to the U.S. government.

Trade attorneys have raised concerns about whether this arrangement aligns with existing export-control statutes. Some experts warn it could invite legal challenges, complicating Nvidia’s already complex China strategy.

Nvidia’s $4 Trillion Milestone and Market Dominance

Despite headwinds, Nvidia’s meteoric rise continues. In June, NVDA stock jumped 17%, briefly outpacing Microsoft in market cap. By July, Nvidia became the first company to surpass a $4 trillion valuation, overtaking both Apple and Microsoft.

Performance metrics remain stellar:

- EPS Rating: 99 (top-level)

- Composite Rating: 98

- 12-Month Outperformance: Nvidia outpaced 87% of all stocks tracked by Investor’s Business Daily.

Still, with an Accumulation/Distribution Rating of D-, fund ownership appears to be cooling, suggesting some caution in institutional buying.

Technical Analysis: Is Nvidia a Buy Right Now?

From a technical standpoint, Nvidia shares are testing their 50-day moving average. The stock remains in a flat base, with an entry point at 184.48. Since this is also the all-time high, buying at this level carries risk but could pay off if Nvidia breaks higher with strong volume.

Investors should watch for confirmation signals before initiating new positions.

Final Thoughts: Nvidia’s Balancing Act Between Growth and Geopolitics

Nvidia remains a juggernaut in AI computing, with unmatched dominance in GPU design, market share, and valuation milestones. However, the company sits at a crossroads. On one hand, geopolitical risks, regulatory hurdles, and competition from Huawei could dampen momentum. On the other hand, Wall Street’s bullish targets, record-breaking revenues, and strategic collaborations reinforce Nvidia’s leadership position.

For investors, the key lies in balancing long-term AI growth potential with short-term political risks. Nvidia may not be a risk-free buy, but its commanding role in AI makes it nearly impossible to ignore.

Reference : VIDYA RAMAKRISHNAN